Find Us

Find Us 1801801

1801801

You make an effort to spend your money wisely – saving where you can and splurging when it’s necessary. However, you’d like to save more and get more benefits – that’s where NBK Rewards Program comes in.

How Can We Help You?

Offers & Rewards

MOST POPULAR

NBK helps you to embrace today while you secure your future. Banking doesn’t have to be boring. Now it’s possible to live in the moment and learn how to save at the same time.

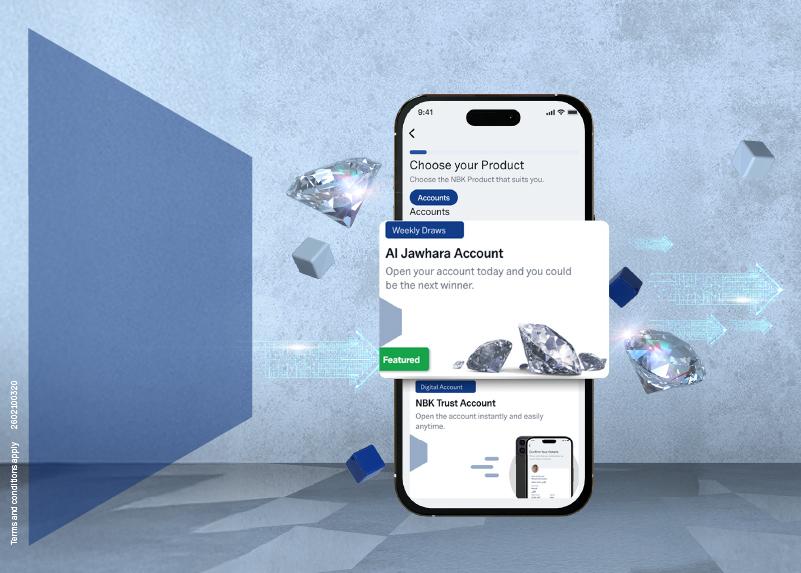

Open Al Jawhara Account today and enter the draw to win Kuwait's biggest prizes.

Apply For An Account

If you are looking to keep your savings safe, you are offered a wide selection of accounts by NBK for your banking needs.

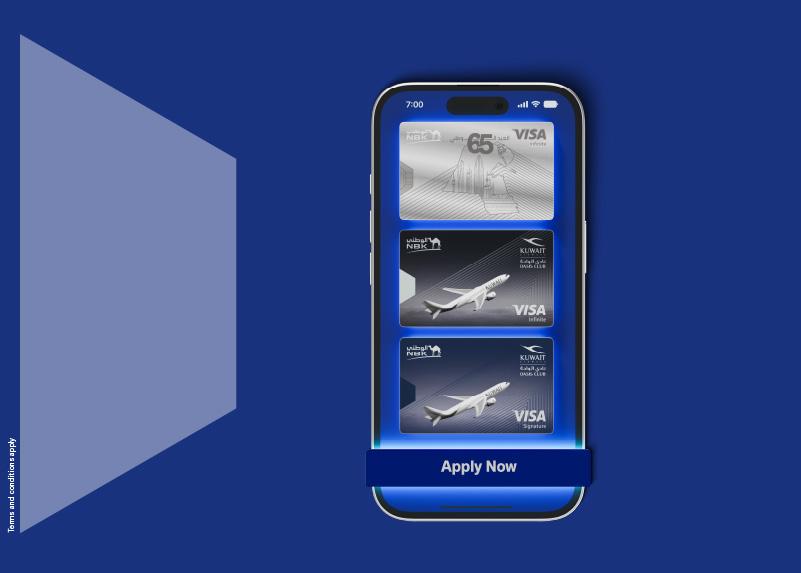

Apply For A Credit Card

If you dream big and reach high then you’ll be sure to find the right NBK Credit Card to help you achieve your goals.

Apply For A Loan

You’re just one step away from satisfaction. All you need is a loan to get to the next phase of your life.

Latest News

24.05.2026

24.05.2026